This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

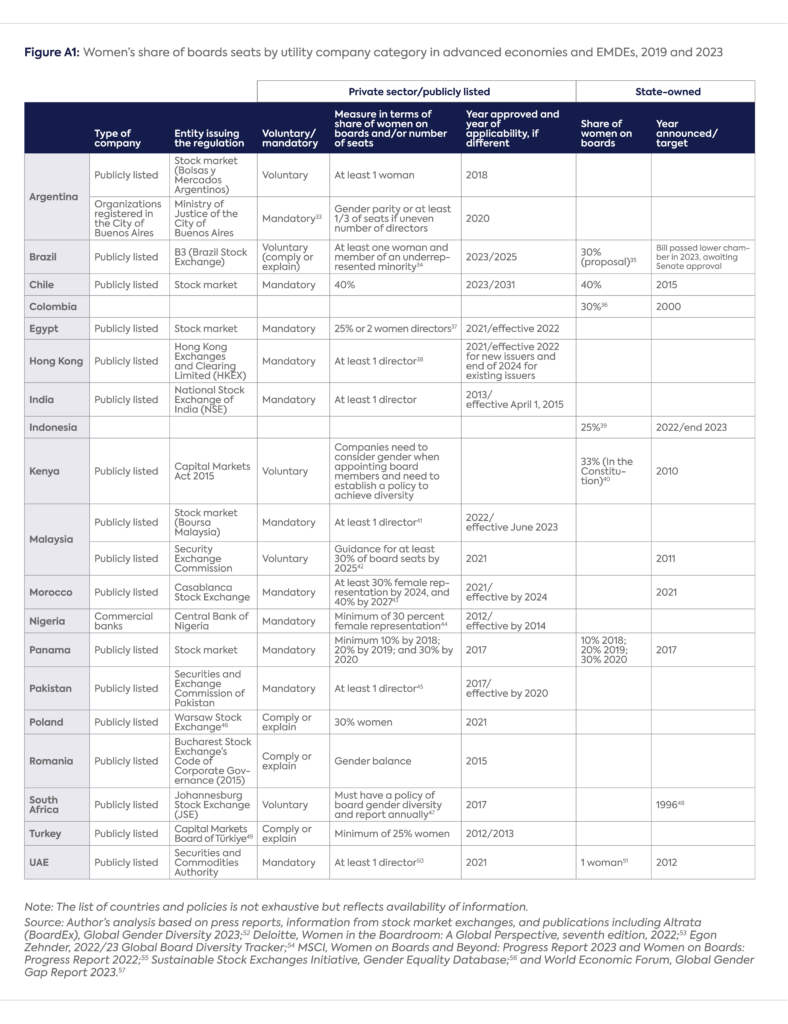

Several emerging markets and developing economies (EMDEs)[i] have taken policy steps in recent years to increase the share of women on companies’ boards of directors, which has the potential to impact the energy sector—historically a sector ranked low by this measure globally, and particularly in EMDEs.[ii] This momentum is noteworthy not only because of the diverse set of countries moving in this direction but also because of the different policy approaches underway. Since 2020, for example, EMDEs as diverse as Chile, Egypt, Hong Kong, Indonesia, Morocco, Pakistan, and the United Arab Emirates have adopted varying policies to increase the share of women on boards (see Appendix A, Table A1, for a full list of countries and types of policies).

What is driving this policy momentum in EMDEs to incentivize and mandate more women on boards (WOB) of companies? The most common rationale cited by regulators from EMDEs is improvements in corporate governance, as studied in academic[iii] and industry[iv] research on the topic. Some regulators have referred to specific aspects of governance, such as overall better decision-making,[v] greater compliance, and lower corruption risks[vi]—the latter a challenging area for EMDEs, in particular those with extractive industries such as oil and gas. Better management of sustainability factors within companies[vii] and alignment with sustainable development goals have also been part of the rationale for mandating WOB.[viii] Another reason cited is pressure from local institutional investor associations,[ix] which coincides with some of the stated engagement positions of global investors about the effect of WOB on governance and long-term performance.[x] In some European EMDEs, mandates for women on boards are coming as a result of EU membership.[xi]

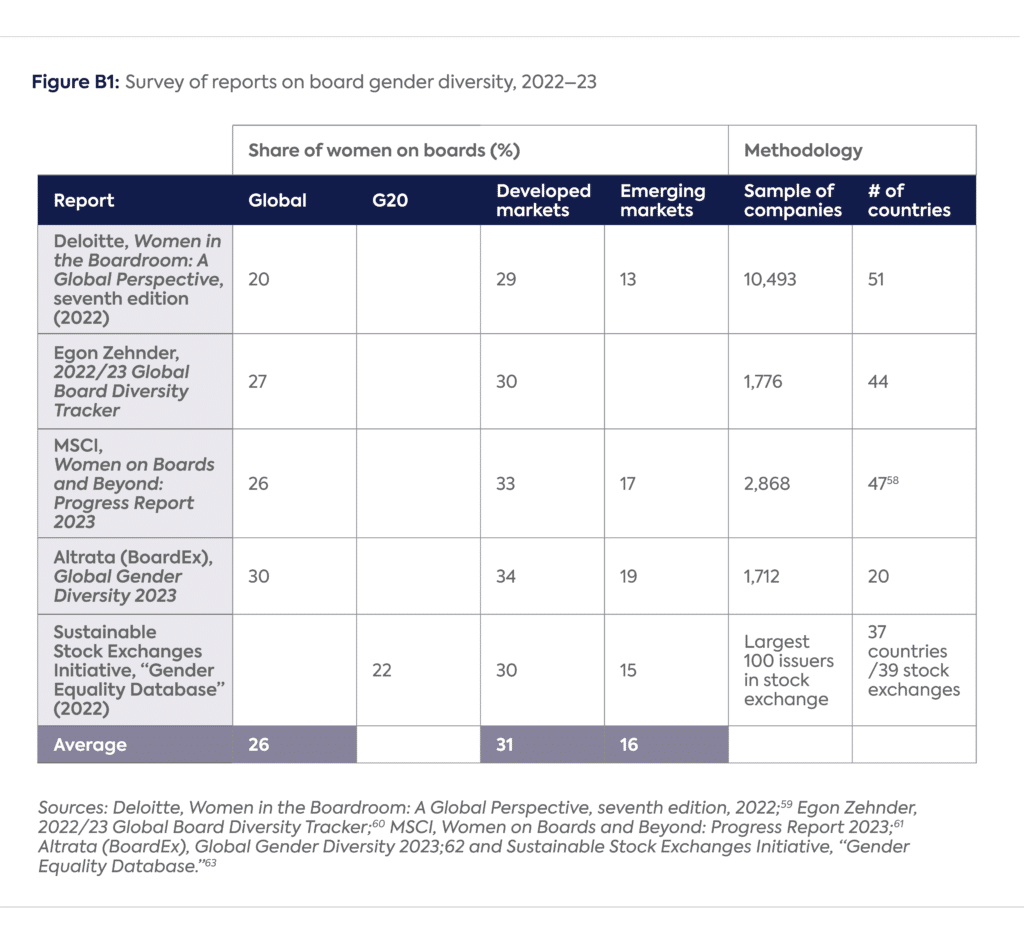

Has this apparent policy momentum in EMDEs made any difference? According to MSCI, a global financial data provider, women occupied 17% of board seats of publicly listed companies in EMDEs in 2023, slightly up from 16% in 2022 but significantly below advanced economies, in which women occupied on average about 33% of board seats in 2023, up from 31% in 2022.[xii] This gap between EMDEs and advanced economies has been increasing, not declining, over time, despite policy action in several EMDEs.[xiii] For energy companies, according to Bloomberg data, the share of women on boards of directors in advanced economies in 2023 was 25%, compared to 14% in EMDEs, lower-than-average levels across all industries as seen in surveys such as MSCI’s (see Appendix B, Table B1, for WOB averages reported in five different surveys).

Given the cited benefits that EMDE policymakers associate with a higher share of WOB, this commentary will look at women’s representation on boards in these countries’ energy companies, a sector associated with governance and sustainability risks. A closer look at companies in this sector reveals overall gaps between EMDEs and advanced economies that have also been increasing over time.

Share of Women on Boards in Energy and Utility Companies: EMDEs versus Advanced Economies

The energy sector, as Bloomberg categorizes it, comprises companies that operate in upstream oil and gas, refining and transportation, storage of fuel products, and natural gas and liquefied natural gas (LNG), as well as integrated oil companies and oil service providers. This sector also includes coal, nuclear, and biofuel companies. For a more complete picture of companies operating in the energy space, the author also analyzed the board makeup of utility companies, which comprise independent power producers, renewable electricity providers, transmission services, and electric and gas utilities. The author examined Bloomberg data on the share of WOB for 1,160 energy companies and 927 utility companies globally.

Before sharing results of this survey, it is worth noting that data on WOB is not comprehensive and therefore the findings in this commentary are estimates. As noted in the figures to come, only about 40% of the companies listed by Bloomberg as energy or utility companies above the market capitalization of $100 million used in this study have any data on board gender diversity. This could mean an overestimation of the representation of WOB. Further, only 33% of EMDE energy and utility companies had data. For advanced economies, about 42% of energy companies and almost 60% of utility companies did. The number of companies included in this commentary, however, is larger than in most general surveys that track WOB for all industries (see Appendix B, Table 1).[xiv]

Despite the data shortcomings, three takeaways are noteworthy:

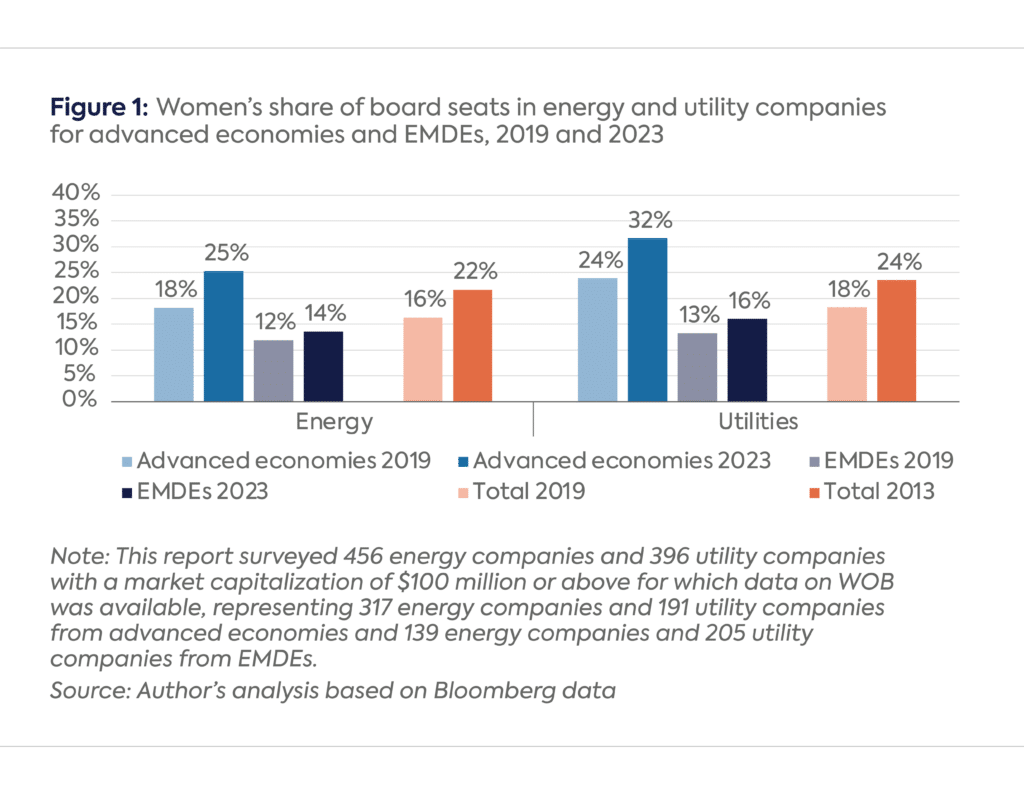

- The share of women on the boards of directors of energy and utility companies has been increasing globally, but that growth masks an important gap between advanced economies and EMDEs.

Women occupied about 22% and 24% of the board seats of energy companies and utility companies, respectively, globally in 2023 (see Figure 1). Given that the average board size for energy and utility companies is about nine and ten directors, respectively, this means an average of about two women directors per board.[xv] However, those averages conceal important differences between advanced economies and EMDEs. Women’s share of board seats for energy and utility companies in advanced economies in 2023 was 25% and 32%, respectively, whereas in EDMEs they were about 14% and 16%. This translates to an 11- and 16-point gap, respectively. And while energy and utility companies from advanced economies have seen a 7- and 8-point increase, respectively, in the share of WOB during the latest five-year period, 2019–23 (inclusive), the share of WOB in EMDEs rose much less. As a result, the gap between advanced economies and EMDEs has been increasing.

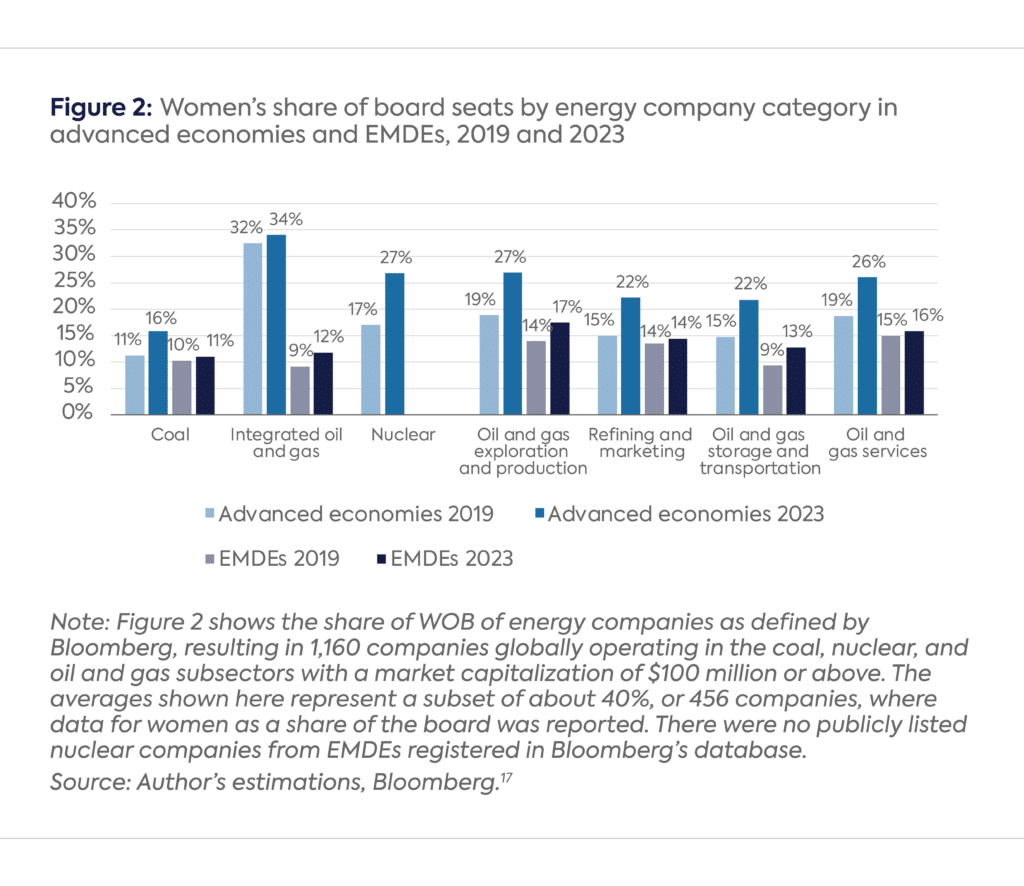

- 2. National oil companies from EMDEs and coal companies globally exhibit the lowest levels of WOB among energy companies.

A closer look at the specific subset of companies that Bloomberg categorizes as belonging to the energy sector reveals that it is in integrated oil companies (present at all stages of the oil and gas production chain) where the largest gap between advanced economies and EMDE companies existed in 2023. At 34%, WOB share in such companies from advanced economies exhibits a 22-point gap with their peers in EMDEs. Most of the integrated oil companies surveyed from EMDEs are national oil companies, and they report 12% WOB, one of the lowest shares in the energy sector. This is all the more relevant in the context of an increasing focus on national oil companies given their growing share of oil, gas, and refining products and thus on their greenhouse gas emissions, part of the sustainability factors policymakers cite as reasons for raising the share of WOB.[xvi]

Coal companies appear to have the lowest share of WOB in the energy sector globally. Notably, this sector also has the lowest gap between EMDEs and advanced economies. Though the representation of WOB in advanced economies has increased since 2019, to 16%, it stands only five points above EMDEs’ 11% (see Figure 2).

Source: Author’s estimations, Bloomberg.[xvii]

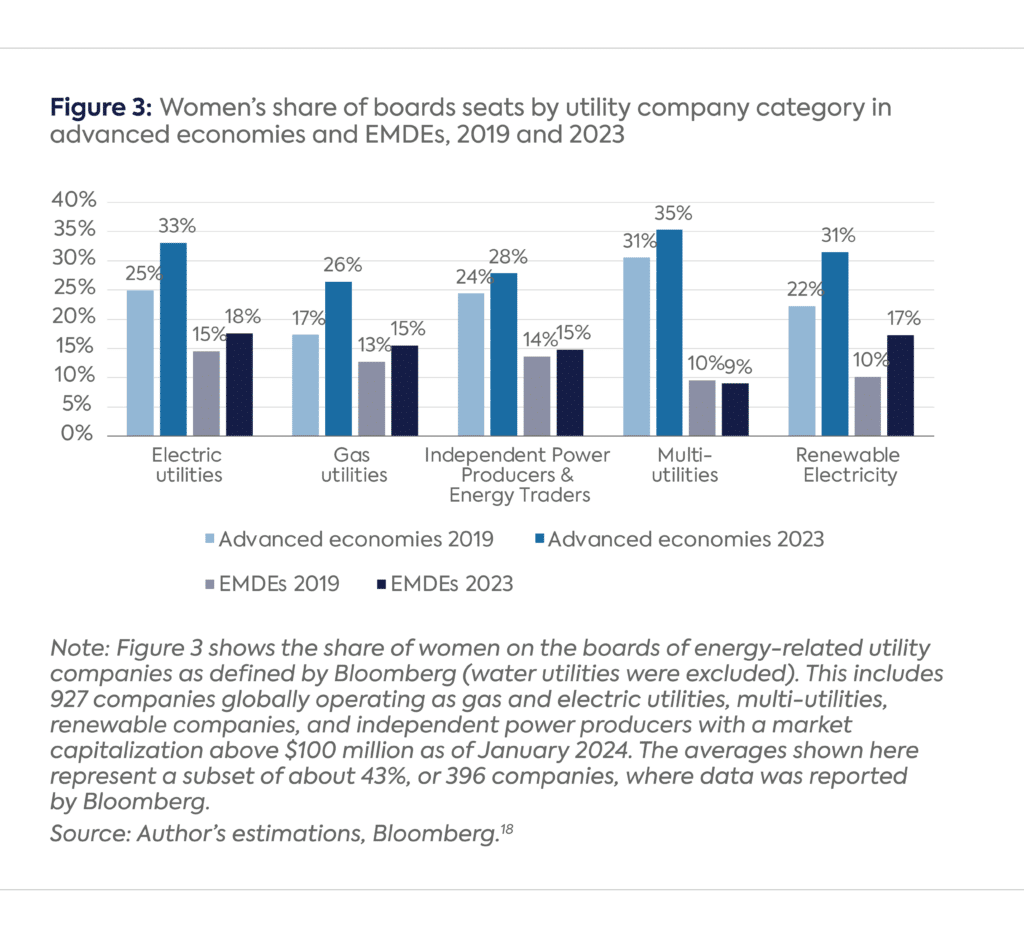

- 3. Utility companies have increased their share of WOB in both EMDEs and advanced economies, to 16% and 32% (Figure 1), respectively, with a notable rise in renewable companies in the past five years.

While women’s share of board seats in most EMDE utilities’ sub-industries has increased since 2019, the marked rise in WOB in advanced economies across utility companies, particularly gas and electric utilities, was not matched, widening the gap (see Figure 3). The gap in WOB share of renewable electricity companies between EMDEs and advanced economies also widened, despite the material rise in the share of WOB of EMDE renewable companies since 2019. The fact that it rose considerably in both, though, could suggest that new energy industries globally might be integrating sustainability criteria faster than legacy ones.

Source: Author’s estimations, Bloomberg.[xviii]

A Policy Push in EMDEs to Address WOB Gaps

Policies to increase the share of WOB of companies in EMDEs have followed different paths. While mandating WOB quotas for publicly listed companies is a known policy approach, EMDEs have also pursued other policies, such as voluntary quotas, guidance by stock markets (or similar regulatory bodies), recommendations in corporate governance codes, and/or mandates for women on boards for state-owned companies.

Mandates for WOB in private-sector companies started in Norway in 2003,[xix] with several other EU countries following suit with quotas focused on publicly listed companies.[xx] India was the first EMDE to pursue such a policy in 2013 (see Appendix A, Table A1).[xxi] Since then, mandates on the share of WOB of publicly listed companies have been adopted by other EMDEs such as Argentina, Egypt, Malaysia, Morocco, Pakistan, Panama, and the United Arab Emirates with different levels of quotas for WOB. In some countries, such as Hong Kong, the goal is to rule out all-male boards by mandating at least one woman board member.[xxii] In others, like Chile and Morocco, the ambition has been as high as having women represent 40% of board seats, albeit with a long transition period of six to eight years.

Several EMDEs have taken a voluntary approach in relation to WOB in companies from the private sector. In some cases, this comes with a nominal quota that issuers in the stock market either need to comply with or explain against doing so, such as in Brazil, Kenya, Poland, Romania, South Africa, and Turkey. This voluntary approach should not be underestimated.[xxiii] Voluntary targets generally also come with required reporting of WOB, which as the previous section underscored remains an issue in many EMDEs.[xxiv] Voluntary mandates might also come with the establishment of diversity criteria in nominating policies for boards, which is the case in Brazil (enacted in July 2023).[xxv] Also, some advanced economies, such as Australia, Canada, New Zealand, and the United States,[xxvi] have followed a voluntary approach, which, along with investor pressure, has been effective at raising the share of WOB.[xxvii]

European EMDEs such as Poland and Romania currently have voluntary approaches, but as part of their EU membership will have to comply with the EU directive issued in 2022 requiring that by 2026 publicly listed companies of member states “have 40% of the underrepresented sex among non-executive directors or 33% among all directors.”[xxviii] This policy will be a much greater challenge for countries such as Hungary that do not have WOB policies. Hungary’s WOB share of 10%, for example, is one of the lowest in Europe; Poland’s is 24%.[xxix]

Mandates for state-owned enterprises (SOEs) have been an interesting policy approach given the large presence of SOEs in EMDEs, particularly in the energy and utility sectors. Kenya enshrined in its constitution a mandate of 33% WOB in its SOEs. Chile, Colombia, Panama, South Africa, and the United Arab Emirates have such mandates for SOEs at varying levels, with Indonesia the most recent country to move in this direction. Brazil is also considering legislation in this regard (see Appendix A).

Chile introduced a novel approach to raising the portion of women on boards last year by issuing a sustainability-linked bond committing to increase the share of WOB in private-sector companies as one of its key performance indicators.[xxx] By 2031, it commits to having at least 40% WOB representation for companies that report to the Financial Regulatory Commission, which includes all companies that issue stocks and bonds—a bold target, as women currently represent about 14% of Chilean corporate board members.[xxxi]

Conclusion

The energy sector exemplifies the large gap in the representation of women on boards of directors between companies from EMDEs and advanced economies. Whether policy efforts in EMDEs to increase WOB will significantly bridge the gap with advanced economies is not clear. At the very least, such policies could help accelerate a rise in WOB in EMDE countries, which continue to fall behind the average of their peers in advanced economies, particularly given the recent directive by the EU mandating 40% WOB by 2026. The regulatory momentum for WOB action by several EMDEs is happening alongside pressures from investors both globally and locally.[xxxii] The inclusion of board diversity as a corporate governance best practice is also raising reputational costs to companies with zero women on their boards.

High-emitting companies globally are under pressure from a multitude of stakeholders on their energy transition risks and opportunities, greenhouse gas emissions footprint, and other risks related to their sustainability performance. EMDE companies, particularly SOEs, might be more shielded from such investor pressure, but they are not immune to it—especially given that the spotlight is likely to increase on these companies in coming years, as most future global emissions growth is expected to come from EMDEs. Greater WOB share in energy companies could be a low-hanging fruit as far as improving corporate governance around exactly the kinds of risks these companies need to navigate in the years ahead.

[i] This report refers to the country classification for EMDEs defined by the IMF and the World Bank in their World Economic Outlook Database. See https://www.imf.org/en/Publications/WEO/weo-database/2023/October/groups-and-aggregates#oem.

[ii] For a comparison of women on boards in different sectors globally, see MSCI, Women on Boards and Beyond: Progress Report 2023, March 1, 2023, 10, https://www.msci.com/research-and-insights/women-on-boards-and-beyond-2023.

[iii] Board gender diversity has attracted considerable academic attention, with studies exploring the impact of women on boards on both financial and non-financial performance. For an example of a study reviewing the existing academic literature on the topic, see Thi Hong Hanh Nguyen, Collins G. Ntim, and John K. Malagila, “Women on Corporate Boards and Corporate Financial and Non-Financial Performance: A Systematic Literature Review and Future Research Agenda,” International Review of Financial Analysis 71 (2020), https://doi.org/10.1016/j.irfa.2020.101554.

[iv] See Moody’s, “Gender Diversity on Boards Linked to Credit Quality, Especially in North America, Europe,”Moody’s Investor Service, March 2023, https://www.moodys.com/web/en/us/about/how-we-work/gender-finance.html#:~:text=Gender%20diversity%20on%20boards%20linked,especially%20in%20North%20America%2C%20Europe%20%C2%BB&text=Higher%2Drated%20companies%20have%20a,parity%20is%20still%20far%20away.

[v] As rationale for their policy, the government of Chile cited a number of studies that showed a higher representation of women in leadership positions bringing benefits such as a “higher return on capital, higher margins, improved financial performance, less corruption, and less fraud … improved risk management, heightened innovation, more diverse opinions, enhanced ability to respond to complex topics, and more involvement in corporate social responsibility.” See Ministry of Finance, Chile, “Chile Sustainability-Linked Bond Framework,” June 2023, 19, https://www.hacienda.cl/english/work-areas/international-finance/public-debt-office/esg-bonds/sustainability-linked-bonds/chile-s-slb-framework-june-2023-version.

[vi] The Pakistan Stock Exchange explains as the rationale for its decision that “better decision making and lower corruption without any compromise on, if not improvement in, the financial performance.” See Securities and Exchange Commission of Pakistan, “SECP Regulation: Women Directors to More than Double in Three Years,” press release, July 8, 2017, https://www.secp.gov.pk/wp-content/uploads/2017/07/Press-Release-July-8-Women-directors-in-Pakistan.pdf.

[vii] Isabel-María García-Sánchez, Sónia Monteiro, Juan-Ramón Piñeiro-Chousa, and Beatriz Aibar-Guzmán, “Climate Change Innovation: Does Board Gender Diversity Matter?” Journal of Innovation & Knowledge 8, no. 3 (2023), https://doi.org/10.1016/j.jik.2023.100372.

[viii] An example of how such measures align with a country’s sustainable development goals agenda is the UAE, which cites “increasing female representation on boards of directors has a positive impact on those boards and their organisations in general, as supported by specialised studies and practical experiences internationally … contributes to achieving the 2030 Sustainable Development Goals, strengthens national governance values and principals, and enhances the country’s global competitiveness.” UAE Gender Balance Council, “Reference Guide for Nomination and Inclusion of Women Board of Directors,” April 2020, https://www.sca.gov.ae/assets/2b9f4422/reference-guide-for-the-nomination-and-inclusion-of-women-on-boards-of-directors.aspx.

[ix] In its press release, Bursa Malaysia cites that the Institutional Investors Council Malaysia (IIC), which comprises large institutional investors, “clearly laid expectations for investee companies to comprise at least 30% women representation on their boards within three (3) years… in line with the large global institutional investors, such as BlackRock, who have started voting against companies with all-male boards.” See Bursa Malaysia, “Bursa Malaysia Applauds Progressive PLCs for Embracing Board Gender Diversity and Censures PLCs with All-Male Boards,” press release, June 2, 2023, https://www.bursamalaysia.com/bm/about_bursa/media_centre/bursa-malaysia-applauds-progressive-plcs-for-embracing-board-gender-diversity-and-censures-plcs-with-all-male-boards.

[x] See, for example, State Street’s “Fearless Girl” board gender diversity stewardship initiative started in 2017, https://www.ssga.com/lu/en_gb/institutional/ic/about-us/what-we-do/asset-stewardship/fearless-girl, and Goldman Sachs’ board diversity initiative started in 2020, https://www.goldmansachs.com/our-commitments/diversity-and-inclusion/board-diversity/2022-update/index.html. This shareholder investor push has been captured by academic research on the impact of investor pressure on women on boards; see Todd A. Gormley et al., “The Big Three and Board Gender Diversity: The Effectiveness of Shareholder Voice,” NBER working paper no. 30657, November 2022 (revised April 2023), https://www.nber.org/system/files/working_papers/w30657/w30657.pdf.

[xi] European Commission, “Gender Equality: The EU Is Breaking the Glass Ceiling Thanks to New Gender Balance Targets on Company Boards,” statement, November 22, 2022, https://ec.europa.eu/commission/presscorner/detail/en/statement_22_7074.

[xii] See MSCI, Women on Boards and Beyond: Progress Report 2023.

[xiii] WOB data by MSCI shows that the gap between companies from emerging markets included in their MSCI EM index and those from advanced companies included in the MSCI world index was about 13 points in 2019 and almost 16 points in 2023. See MSCI, Women on Boards and Beyond: Progress Report 2023, 7, Exhibit 1.

[xiv] The averages contained in this report resulted from 456 energy companies and 396 utility companies for which data on WOB was available, representing 321 energy companies and 191 utility companies from advanced economies and 139 energy companies and 205 utility companies from EMDEs.

[xv] The average global size of boards was 9 directors for energy companies according to a sample of 470 companies in the energy industry and 10 board seats for utility companies out of a sample of 258 companies for which data was reported by Refinitiv, accessed March 20, 2024.

[xvi] Luisa Palacios and Catarina Vidotto Caricati, “Assessing ESG Risks in National Oil Companies: Transcending ESG Ratings with a Better Understanding of Governance,” Center on Global Energy Policy, Columbia University, May 2023, https://www.energypolicy.columbia.edu/publications/assessing-esg-risks-in-national-oil-companies-transcending-esg-ratings-with-a-better-understanding-of-governance/.

[xvii] Bloomberg Equity data, screening all energy, percent women on board, calendar years 2019–23 subindustry names and country and territory, accessed February 28, 2024.

[xviii] Bloomberg Equity data, screening all utility, percent women on board, calendar years 2019–23, subindustry names and country and territory, accessed March 4, 2024. Water utility companies were excluded.

[xix] Marianne Bertrand, Sandra E. Black, Sissel Jensen, and Adriana Lleras-Muney, “Breaking the Glass Ceiling? The Effect of Board Quotas on Female Labor Market Outcomes in Norway,” NBER working paper no. 20256, June 2014 (revised July 2017), https://www.nber.org/papers/w20256.

[xx] Spain introduced gender quotas for corporate boards in 2007; Belgium, France, Italy, and the Netherlands in 2011; Germany in 2015; Austria and Portugal in 2017; and Greece in 2020. All of the quotas are expressed in terms of share of total board seats, with France, Italy, and Spain requiring women to hold 40% of corporate board seats, followed by 33% for Belgium and Portugal; 30% for the Netherlands, Germany, and Austria; and 25% for Greece. See Policy Department for Citizens’ Rights and Constitutional Affairs, Directorate-General for Internal Policies, European Parliament, “Women on Boards Policies in Member States and Their Effects on Corporate Governance,” December 2021, http://www.europarl.europa.eu/RegData/etudes/STUD/2021/700556/IPOL_STU(2021)700556_EN.pdf.

[xxi] Ruth V. Aguilera, Venkat Kuppuswamy, and Rahul Anand, “What Happened When India Mandated Gender Diversity on Boards,” Harvard Business Review, February 2021, https://hbr.org/2021/02/what-happened-when-india-mandated-gender-diversity-on-boards.

[xxii] The Hong Kong Stock Exchange (HKEX) first ruled no new issuers with all-male boards as of 2023, with all listed companies required to comply by 2024. See Hong Kong Stock Exchange, “Exchange Publishes Conclusion on Review of Corporate Governance Code,” press release, December 10, 2021, www.hkex.com.hk/News/Regulatory-Announcements/2021/211210news?sc_lang=en.

[xxiii] Heike Mensi-Klarbach, Stephan Leixnering, and Michael Schiffinger, “The Carrot or the Stick: Self-Regulation for Gender-Diverse Boards via Codes of Good Governance,” Journal of Business Ethics 170 (2021), https://doi.org/10.1007/s10551-019-04336-z.

[xxiv] While lacking voluntary quotas for WOB, some EMDE countries have begun to require disclosures of board gender diversity as a measure to incentivize and promote board diversity. One example is South Africa: the Johannesburg Stock Exchange recently adopted a specific requirement for listed companies to disclose targets for gender and race representation at the board level. See Deloitte, Women in the Boardroom: A Global Perspective, seventh edition, February 2022, https://www2.deloitte.com/sg/en/pages/risk/articles/women-in-the-boardroom-global-perspective-seventh-edition.html.

[xxv] Brazil’s “comply or explain” rule also contains a requirement for companies to include diversity criteria in the nomination process for boards of directors and C suites, contained in the Brazilian stock market’s ESG annex. See https://www.b3.com.br/data/files/3B/31/0A/CF/394798101DBF7498AC094EA8/Regulamento%20de%20Emissores%20_20.07.2023_.pdf.

[xxvi] There are no federally mandated rules for publicly listed companies in the US. However, the Nasdaq issued a regulation in 2021 that at least one woman or another minority serve on the board of directors of listing companies by the end of 2023 (for new listings, this applies for the end of 2024). See Andrew Ramonas, “Contested Nasdaq Board Diversity Rules Take Effect: Explained,” Bloomberg, December 21, 2023,

https://news.bloomberglaw.com/esg/contested-nasdaq-board-diversity-rules-take-effect-explained. Several states have adopted quotas for gender diversity on boards of companies and other organizations, including California; the California law was overturned by the lower courts.

[xxvii] For example, the US saw an increase in the share of WOB from an average of 26% in 2019 to 32% in 2022. OECD Employment Database, “Female Share of Seats on Boards of the Largest Publicly Listed Companies,” accessed March 5, 2024, https://stats.oecd.org/index.aspx?queryid=54753.

[xxviii] European Commission “Gender Equality: The EU is Breaking the Glass Ceiling Thanks for New on Gender Balance Targets on Company Boards.”

[xxix] OECD Employment Database, “Female Share of Seats on Boards of the Largest Publicly Listed Companies,” accessed March 5, 2024.

[xxx] Ministry of Finance, Chile, “Chile Sustainability-Linked Bond Framework.”

[xxxi] Ibid., 18.

[xxxii] Gwladys Fouche, “Norway’s Wealth Fund Pushes for More Women on Emerging Market Company Boards,” Reuters, March 6, 2024, https://www.reuters.com/sustainability/society-equity/norways-wealth-fund-pushes-more-women-emerging-market-company-boards-2024-03-06/; Ross Kerber, “State Street Calls for Women on Corporate Boards Worldwide,” Reuters, January 12, 2022, https://www.reuters.com/business/state-street-calls-women-corporate-boards-worldwide-2022-01-12/.